How Can I Prepare for a Market Correction?

The U.S. equity market has been in a solid uptrend since the announcement of successful vaccine trials last November. However, this type of market behavior is somewhat abnormal – over the past 41 years, the S&P 500 has fallen by an average of 14.3% during the course of the year, but in 31 of those 41 years has gone on to finish the year in positive territory. Put simply, equity markets are resilient, but volatility is normal.

In general, questions about market corrections are really questions of when, rather than if. There is a lot of good news priced into the equity market today, and it would not be surprising to see volatility begin to rise as investors shift their focus from an economy that is reopening to a less certain growth outlook and tighter monetary policy. However, in a world where stocks remain cheap relative to bonds, and it remains unclear as to whether high quality fixed income will provide the type of protection it has historically, where can investors look in the equity market to seek shelter during periods of volatility?

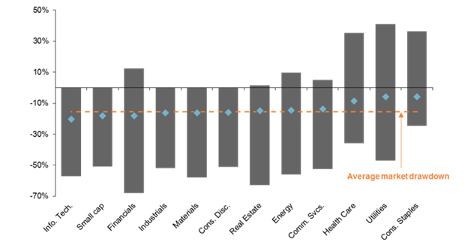

As shown in the chart below, some sectors tend to experience sharper drawdowns on average than others during periods of market stress. Specifically, and perhaps unsurprisingly, health care, utilities, consumer staples, and communication services have all historically outperformed the broader market in these environments. On the other hand, the more cyclical parts of the market like financials and small caps have been hit quite hard.

That said, the devil is always in the details. For example, average drawdowns for the technology sector are skewed by the tech bubble, while the energy sector saw positive returns during periods of market stress on two occasions since 1995. Furthermore, financial stocks rallied more than 10% as the Tech Bubble deflated and the technology sector fell by more than 50% in 2000. This means that it is important to understand historical relationships, but also look for signs of where idiosyncratic risks may be building.

In the current environment, valuation is the elephant in the room. We took a look at the average valuation by sector just before the largest decline in any given calendar year, and found that the sectors which have seen the largest drawdowns also tend to be the most expensive going into those drawdowns. As such, investors may want to focus on the intersection of valuation and historical volatility when positioning equity portfolios for what could be a bumpy ride this summer.

Sector dispersion during equity market drawdowns

Historical range vs. average, 1995 – present

Source: FactSet, J.P. Morgan Asset Management. Average market drawdown is calculated using the maximum drawdown in the S&P 500 price index on a calendar year basis. *Real estate calculations are since 2002, due to a lack of available data. Data are as of June 1, 2021.

Monthly child tax credit payments start July 15. Here’s what parents need to know

PUBLISHED TUE, JUN 15 202110:33 AM EDTUPDATED TUE, JUN 15 202112:34 PM EDT

In just a few weeks, monthly child tax credit payments will go out to U.S. households that are home to about 65 million kids, according to the IRS.

The expanded child tax credit was established in the American Rescue Plan signed into law in March. In 2021, the maximum enhanced child tax credit is $3,600 for children younger than age 6 and $3,000 for those between 6 and 17.

The credit will be distributed as an advance on 2021 taxes in monthly installments. For households getting the full benefit, those payments will be $300 per month for children under the age of 6 and $250 for those between the ages of 6 and 17.

Here’s what families need to know ahead of the July 15 start.

More from Invest in You:

Some families may want to opt out of child tax credit payments starting in July

This researcher hopes to change Biden’s mind about student loan forgiveness

As travel demand surges and prices rise, 7 saving tips for this summer

Who qualifies for the maximum credit?

Most American families qualify for some amount of money.

The full credit is available to married couples who file taxes jointly and have children and adjusted gross income less than $150,000, or $75,000 for individuals. The enhanced tax credit will phase out for taxpayers who make more money and cease for individuals earning $95,000 and married couples earning $170,000 filing jointly.

Taxpayers who make more than that will still be eligible for the regular child tax credit, which is $2,000 per child under age 17 for families making less than $200,000 annually, or $400,000 for married couples.

What do I need to do?

Most eligible families don’t have to do anything right now, according to the IRS. The agency will use 2020 tax returns to determine eligibility or 2019 returns for those who haven’t filed taxes for last year.

In early June, the IRS started sending out 36 million letters to families who many be eligible for the credit and monthly payments.

Those families that traditionally don’t file taxes because they don’t have enough income but have children in their household who are eligible can now sign up for the benefit. On June 14, the IRS started a portal for nonfilers to register to receive the new credit.

If your family had a change in circumstance in the last year, that may mean you are eligible for a larger payment, or if you need to change where the benefit should be sent, the IRS will open another portal in June to give the agency that updated information. This includes having a baby, a large change in income or needing the payment to go to a different parent than claimed the child in 2020 (or 2019, if that’s the last tax return you have on file).

How will payments be sent?

As with the stimulus checks sent out by the IRS earlier this year and in 2020, most of the monthly child tax credit payments will be sent by direct deposit — some 80% of those eligible will get the money this way, according to the agency.

If the IRS has direct deposit information on your tax return, that is likely how you’ll receive the monthly credit. If you don’t have direct deposit, the IRS will also be sending out paper checks to some families.

When will future payments be sent?

The IRS said that future payments will be made on the 15th of each month, unless the 15th falls on a weekend or holiday, at which point the money will be sent on the closest business day. After the benefit first goes out July 15, families can expect subsequent payments on Aug.13, Sept. 15, Oct.15, Nov. 15 and Dec. 15.

So far, the monthly payments are only scheduled to continue through the end of 2021. Families will receive the second half of the credit when they file their 2021 taxes in 2022. But that could change — President Joe Biden has suggested making the enhanced credit available through 2025, and other Democrats want to make it a permanent benefit.

Can I opt out? What happens if I do?

Families can opt out of receiving the monthly payments for the credit through an IRS portal set to start in June. Those who do this won’t get the monthly amounts but will still receive the full credit they are eligible for when they file their 2021 taxes.

Some families may choose this route because they don’t need the monthly payments immediately or prefer to get a large lump sum of money back from the IRS as a tax refund, said Elaine Maag, a principal research associate at the Urban-Brookings Tax Policy Center

“There’s evidence that shows that some people really like getting that large tax refund, and can use it as an opportunity to purchase a large household item like a refrigerator or put together first and last month’s rent so they can move,” she said.

Did you Know?

CASH ONLY

– Total US credit card debt peaked at a record $930 billion as of 12/31/19 (pre-pandemic) but has since fallen 17% ($157 billion) to $773 billion as of 3/31/21 (source: Federal Reserve Bank of New York).

HELP WANTED

– The number of job openings in the USA climbed to 9.3 million at the end of April 2021, the highest number ever recorded and up +1.0 million in just the last month. By comparison, at the depths of the mortgage crisis, there were 2.1 million job openings available in July 2009 (source: Bureau of Labor Statistics).

Quotes:

Finally, all of you, be like-minded, be sympathetic, love one another, be compassionate and humble. – 1 Peter 3:8

“Be the change you wish to see in the world.” -Gandhi

The views stated in this letter are not necessarily the opinion of Cetera Advisor Networks LLC and should not be construed directly or indirectly as on offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past Performance does not guarantee future results.