Reading the Signals on Inflation

Economic activity is surging in the United States as vaccination rates rise and more areas of the economy re-open. With this positive news, however, comes concern of inflation. Enormous pent-up demand for goods and services, fueled by historic levels of stimulus, may not be met with sufficient supply, as many businesses are still recovering from the pandemic shock. While markets have anticipated some of these pressures—seen via rising inflation expectations and U.S. Treasury yields—explosive price movements in supply-impaired areas like lumber raise the question: Could the market be underappreciating the possibility of a sustained rise in inflation? At the same time, investors are mindful of larger structural trends, such as globalization and innovation, that have kept inflation low for decades despite prior bouts of inflation concerns.

While “this time is different” may be viewed as a hubristic cliché, the fact remains that today’s circumstances are without historical parallels. Never have we experienced such a reversal in consumer demand, from depressed levels because of the pandemic, to a rapid resurgence as stimulus and vaccine effects are felt. Moreover, the U.S. Federal Reserve (Fed) has indicated a substantial shift in its approach to inflation. With limited history to guide us, investors are right to wonder what they can truly expect, and how worried they should be.

On March 20, Procter & Gamble, one of the largest producers of consumer staples in the world, joined a growing group of companies that are signaling price hikes for certain products. Shortages in key inputs, such as lumber and semiconductors, have contributed to rising home construction prices and fierce competition for used cars. Many employers report difficulty in hiring to meet demand.

Each of these instances is indicative of a classic supply/demand imbalance that typically leads to inflation. Put simply, until there is enough of what people want, the price rises until we reach an equilibrium—and that price-rise is inflation. When it costs us more to get something than it used to, the purchasing power of our hard-earned dollar has declined.

Only Temporary?

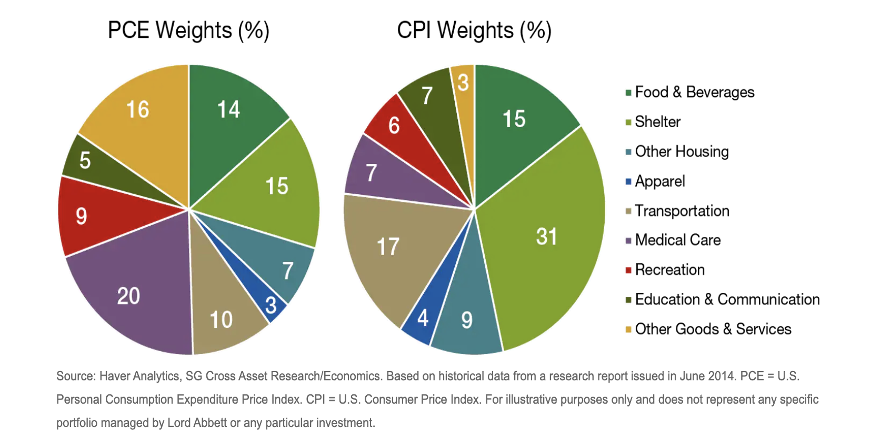

However, price increases in highly visible areas do not necessarily mean broad-based degradation of purchasing power, nor are those price increases necessarily persistent. For example, we may have a temporary shortage of chips, leading to a short-lived stall in vehicle production, but eventually those chips will get back to normal production, and supply will catch up to demand. So, this situation of surging prices and shortages, while alarming, is not necessarily indicative of a permanent inflationary problem. Moreover, consumer products are only one piece of the inflationary puzzle. Take a look at Figure 1, which depicts the composition of two key inflation gauges: the consumer price index (CPI), which focuses on what households are buying and determines social security increases and TIPS valuations, and the personal consumption expenditure (PCE) index, which is based on a survey of what businesses are selling and is the preferred inflation metric for the Fed.

Figure 1. History Shows There’s Much More to Inflation than Prices of Consumer Goods

As the chart shows, housing, medical care, transportation, and even recreation play at least as much of a role in calculating inflation as consumer goods. Many current economic forecasts expect only a small impact to CPI or PCE from these expected increases. However, we can also see reasons for upward pricing-pressures in each of these other areas: housing prices and rents are rebounding sharply; vehicle prices and energy costs are rising, while a demographic shift out of urban areas may sustain these pressures; medical costs have been rising for years as Baby Boomers continue to age; and so on. Markets have clearly responded to this potential, and investors now expect inflation to run higher for the next few years than it has run for the past two decades. However, the uptick in inflation expected by markets is still relatively modest, and markets expect this trend to last only a few years.

Certainly, demand and supply balance out over time. We are likely to see more volatility in high-demand areas over the short term, but such imbalances are always transitory. Has something fundamentally changed to keep inflation higher? We would say the answer is “maybe.” Markets can ultimately shrug off short-term phenomena, but persistent inflation has the potential to meaningfully affect asset prices, while potentially forcing the Fed to change course. The Fed’s explicit shift in its approach to inflation, announced in October 2020, means that it will be slower to react to any increase in inflation, perhaps permitting price pressures to persist against a backdrop of massive fiscal spending that has the potential to fundamentally increase aggregate demand for goods and services. And finally, the pandemic has changed so many aspects of life that there may well be some unforeseen dynamics that alter the low-inflation regime we have been in for decades.

A Final Word

That said, history shows that it is difficult, if not impossible, to predict the trajectory of inflation with any degree of accuracy. What we do know is that companies and investors have been trained to believe inflation potential is limited. Markets and the economy have been set up to operate in a low-inflation world, so there are clear risks to the status quo if inflation does prove more persistent than current expectations. We also know that we are certain to see more supply/demand imbalances shooting prices higher in the coming months as demand comes surging back.

While it would be overly simplistic to extrapolate specific areas of price increases into a broader inflation trend, it would be foolhardy to ignore them, and the potential for that volatility to spill over into broader markets, or for seemingly temporary moves to become more permanent than many analysts anticipate. Investors should reasonably ask if they are being appropriately compensated for this inflation uncertainty, or how best to protect themselves. While there are no easy answers, we will continue to monitor inflation closely in the months to come.

Paulson, Timothy. “Reading the Signals on Inflation.” Lord Abbett, 3 May 2021

Unsustainable

The US economy is recovering rapidly from COVID-19. The rollout of vaccines, the lifting of restrictions, loose monetary policy, and a massive increase in government spending are all playing their parts. The problem is that the massive government “stimulus” checks have put the economy in a strange position, where retail sales are far above where they would be if COVID had never happened, even as the production side of the economy remains relatively weak.

Friday’s report on the retail sector showed that retail sales were unchanged in April, remaining at essentially the same lofty level they were in March. However, the lack of an increase in April shouldn’t have been much of a surprise. Even with no increase in April, retail sales were 17.9% higher than they were in February 2020, pre-COVID. To put this in perspective, that’s the fastest gain for any 14- month period since 1978-79. A key difference? That period in 1978-79 had double-digit inflation, versus the 3.1% increase in consumer prices since February 2020.

Another way to think about how high retail sales have been lately is that if COVID had never happened and sales since February 2020 had increased at a more normal 4.5% per year pace, it would have taken until November 2023 for retail sales to reach where they were in March and April this year. In other words, sales have arrived at the recent level about two and half years ahead of schedule. This means that growth in retail sales will face a headwind over the next few years as the extraordinary recent bouts of “stimulus” peter out, roughly offsetting the benefits of more jobs and higher wages.

Meanwhile, even though retail sales have surged to abnormal highs, the production side of the economy is still operating below pre-COVID levels and even further below where production would be today if COVID had never happened. Manufacturing production is down 2.7% versus February 2020. Part of this is damaged supply chains. The demand for new cars and trucks has rarely been higher. Retail spending at auto and motor vehicle dealerships was 33.1% higher in April than in February 2020. And yet motor vehicle production (excluding parts) is down 18.1% versus February 2020, largely due to a shortage of semiconductor chips. But it’s not only autos. Manufacturing excluding autos is down 0.9% versus February 2020.

In spite of the hopes of some policymakers, the economy doesn’t work like a light switch. It’s not just sitting there waiting for some public officials to turn it on, returning it to pre-COVID normal operation. Many businesses have disappeared, never to return, and many of them had a huge store of operational and knowledge capital built into them, know-how about the best way to get certain things done, that capital having been developed over decades.

The divergence between consumer spending and actual production is a manifestation of inflationary economic policies, which also showed up in last week’s reports. Consumer prices are up 4.2% from a year ago while producer prices are up 6.2%. That’s what you get when people are spending more dollars provided by short-term oriented government policies, not the return for the production of actual goods and services.

But, ultimately, there is no free lunch. All extra government spending today must be paid for by reduced spending by others, today or in the future. For now, there are plenty of reasons to remain bullish. Opening up is the best stimulus and the economy still has long way to go to get fully open. Look for further gains in production in the year ahead, even if there are some potential headwinds brewing in the long-term.

Wesbury, Brian S., et al. “Unsustainable.” First Trust Monday Morning Outlook, 17 May 2021

Did you Know?

WOOD

– The average cost of building a new single-family home in the US has increased by +8% in the last year ($24,000) solely because of the rising cost of lumber. Lumber mills shut down nationwide in 2020 for as long as 4 months, leading to a lumber shortage as homebuilding demand accelerated. Lumber imports into the USA have been impacted by a beetle plague ravaging Canadian forests (source: National Association of Homebuilders).

BUCKS FROM THE GOVERNMENT

– Pandemic stimulus payments to individuals and federal unemployment benefits made up 22% of the record-setting US personal income total reported by the government for March 2021. The same 2 categories made up just 3% of national personal income in January 2020, i.e., immediately before the pandemic began (source: Bureau of Economic Analysis).

Quotes:

“Financial fitness is not a pipe dream or a state of mind. It’s a reality if you are willing to pursue it and embrace it.” – Will Robinson

“Don’t judge each day by the harvest you reap but by the seeds that you plant.” – Robert Louis Stevenson